Unlocking Innovation for Banks Begins with Legacy Modernization

By Team Eela on May 26th, 2023

Today users expect banks to provide the same kind of in-built services and features that they regularly get from entities on the leading edge of digital innovation, such as e-businesses and others. Furthermore, the BFSI vertical provides a stiff advantage to banks through their fast-paced services and customer-friendly products.

With the quickly growing market tactics and changing user expectations, legacy systems no longer support banks. Moreover, the maintenance and operation of the old systems become even more costly and critical as we advance. Hence, implementing modernization at a later stage impacts profitability and makes survival easier.

Through this guide, you will understand the concept of legacy banking or modernization- the need, benefits, best practices, and helpful technologies. Let’s dive in!

Defining the Term “Legacy Modernization”

Legacy modernization refers to updating or replacing outdated software, hardware, or business processes with newer, more efficient technology solutions. Outdated systems often need to be updated, easier to maintain, and burden organizations that rely on them. This is where legacy modernization comes into play as they replace or upgrade legacy systems with modern technology solutions.

The modernization process can take many forms, including re-platforming, re-hosting, re-engineering, or complete replacement. Re-platforming involves migrating the legacy system to a new platform while re-hosting consists in moving the legacy system to a new hosting environment. Re-engineering involves rewriting or modifying the legacy system’s code to make it more efficient and easier to maintain, while complete replacement consists in developing a new system from scratch.

Legacy Banking System Modernization Significance

Age-old systems are critical and bring challenges to banks. Some of the reasons why the modernization of the banking legacy system is significant:

Compatibility: Mobile & online banking features, speed of services, and other broad range of products are immensely changing users’ choice of bank. Legacy software must be compatible enough to cope with rapidly evolving customer expectations.

Speed: New-age users wish to make payments, complete transactions, or open a bank account quickly. But with the legacy banking system, every process becomes arduous and lengthy.

Security: Security protocols of legacy banking systems lack appropriate tech updates and support. So, banks having legacy systems are vulnerable to security breaches. This is significant because it makes them incapable of adhering to regulatory compliance needs. In addition, as users believe their money is with the banks, age-old software decreases reliability.

Growth: Banks cannot get the future-ready as the mechanism behind the time makes it impossible to provide modernized products and services. It causes a loss of their current position and growth in the industry.

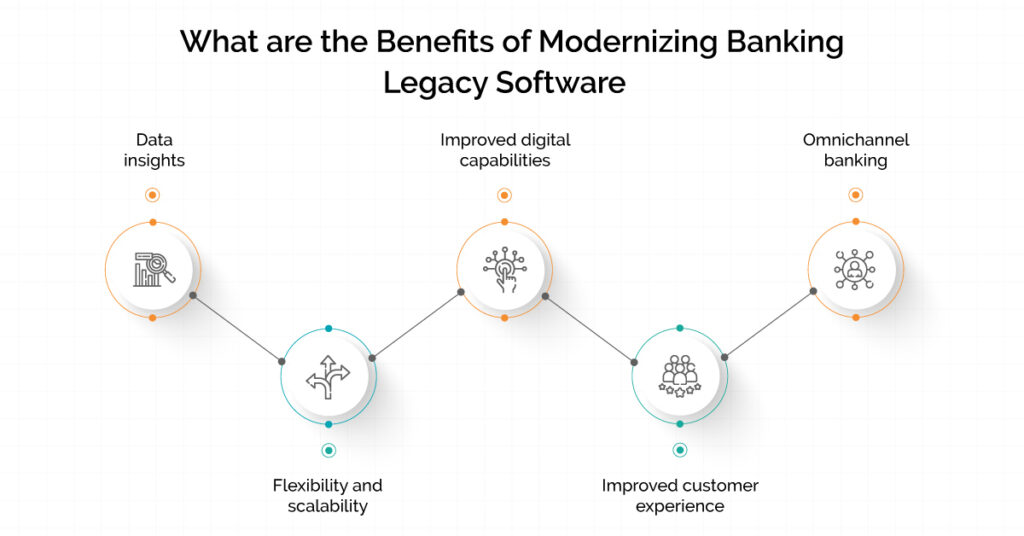

What are the Benefits of Modernizing Banking Legacy Software

Data insights: Modernizing legacy banking systems support banks in extracting legacy institutional information and offers modernized data analytics to give a competitive benefit. It provides actionable insights about improvement opportunities and areas, leading to effective decision-making and attaining business objectives.

Flexibility and scalability: Although legacy banking restricts the growth of banks, technologies such as artificial intelligence, cloud computing, machine learning, and others ensure users enjoy scalability and flexibility across the value chain.

Improved digital capabilities: Advanced software can integrate modern capabilities to support banks to remain compatible with Application Programming interfaces (APIs). It incorporates the latest technology, such as machine learning, artificial intelligence, and others, to allow banks to sustain the rapidly changing demands of the industry with digital capabilities and features.

Improved customer experience: Modernizing legacy banking monetary unit help enhance the banking service facilities, promotes product innovation, and offers quick, seamless user onboarding. It also saves customers from crashes and slowdowns linked with age-old software while providing a better customer experience.

Omnichannel banking: With modern technology, banks can offer omnichannel experiences by enabling users to carry out the same operations through a bank branch, call center, mobile phone, and online banking. For example, a user can start the onboarding procedure online and complete it through a call center.

Best Practices to Follow for Modernizing Legacy Banking Software

Some of the standard practices to incorporate into your system are:

Analyze your legacy system and compute its technical debt: This began by knowing where your core unit is coming under the current market standards. Predominantly, legacy systems suffer due to low-quality bugs or code because of the long-term project managed by several developers over time. Hence, it measures the technical debt while analyzing the features, functions, and upgrade requirements.

Get involved in the process and examine the options: Understanding the complexities and costs integrated with the project is crucial. Your company can take support from fintech software development organizations to learn about the right strategy for modernizing legacy banking software. This helps the core decision-making team work closely with the IT team and offer related inputs to shape the solution effectively.

Keep your business goals at the focus: Emphasize the company aims and strategic advantages you wish to achieve by updating core software. It helps to develop and enhance business values. Hence, evaluate risk, define measurable goals, and set tolerance by discussing them with the IT team to ensure the work progresses as planned.

Prioritize data security: Banks have confidential financial data of several account holders. In addition, they have integrated huge intellectual assets and valuable information over the years. Hence, confirming complete data security throughout the software transition is significant.

Become future-ready: Choose the technology that will stay relevant and compatible for several years. An experienced IT partner offers a practical suggestion about deployable architecture. Select a highly flexible and scalable software stack to allow further improvement with small iterations cost-effectively.

Ensure seamless accommodation of revamped system: This level is tricky as even effective software can fail. Therefore, you need to prepare your software in advance with the IT team. Train workers, know about the maintenance and update schedules, and casually anticipate occurring incidents and prepare for them.

Insight into Common Modernizing Legacy Banking System Technologies

Cloud computing: Cloud computing services help banks to adapt to the changing market environment and offer flexibility to their products and services. Without significant investment, the bank can manage data and applications in remoter servers and abruptly scale resources while enhancing operational efficiency.

Low code development: It helps to decrease the delivery time. It demands minimal coding to add valuable improvements concerning processes and applications to legacy units.

Chatbots: They provide online conversations with individuals while improving their experience with banks. Replying to user issues and queries 24/7, help banks maintain their reputation by avoiding online reviews. They also help consumers with their banking responsibilities and offer personalized services.

APIs: Banks should be a part of digital ecosystems to sustain in the rapidly changing dynamics. They should enable you to receive money transfer requests from digital payment systems, card systems, mobile wallets, and third-party financial services. In addition, modernizing legacy banking system efforts must include APIs as they allow apps and software to share data and communicate.

Advanced data analytics through big data: Banks benefit from big data as they are data-intensive institutions and collect data from several sources, such as online transactions, KYC, ATMs, etc. Modernized data analytics provide personalized services and actionable insight

Process automation with AI-ML-RPA: Digital process automation helps banks to scan and reduce chances of sanction screening and anti-money laundering, commercial lending operations, stick with regulatory compliance, letter of credit & guarantees, trade finance, and others.

Conclusion

In the ever-rapidly changing digital world, the time to follow legacy systems is long gone. The reformed industry has no option but to implement a modernized banking system.

Modernizing the legacy banking software help banks improve product and service quality, attract new customers, and unlock profitable revenue streams.

WRITTEN BY

Team Eela

TechEela, the Bedrock of MarTech and Innovation, is a Digital Media Publication Website. We see a lot around us that needs to be told, shared, and experienced, and that is exactly what we offer to you as shots. As we like to say, “Here’s to everything you ever thought you knew. To everything, you never thought you knew”