How Advanced Analytics Helps Banks in Fraud Detection

By Team Eela on April 19th, 2023

The fraud detection analytics procedure in the banking and financial sector has always been challenging. Imposters are becoming more aware daily, making it tough to detect fraudulent activities without using advanced analytics techniques like machine learning and artificial intelligence.

In this guide, we will discuss the use of machine learning in the banking sector and explore the benefits of advanced analytics for fraud detection. Keep reading!

Defining Fraud Detection and its Significance

Fraud detection refers to identifying and preventing fraudulent activities or behaviors within a system or organization. Fraud detection aims to identify and prevent fraud before it causes financial loss or other negative consequences. Hence, fraud detection analytics has become significant across different sectors.

The technique used to detect fraud differs based on the case. The entire responsibility lies on the data analysts and specialists with a brief in risk assessment. Although, manual verification is time-consuming and labor-intensive. Thus, fraud detection using data analytics typically involves various techniques such as data analysis, pattern recognition, and machine learning algorithms to detect suspicious activities or transactions that may indicate fraud.

How do Fraudsters Function, and What are the Common Types of Fraud?

The nature of fraud varies from case to case. Some involve identity theft or illegal takeovers, commonly requiring industry insight or organized criminal activity: another, less severe one which might not impact the company’s image but its financial safety.

Fraudsters function either on their own or in organized groups. The groups are the toughest to identify as they possess mixed insights and dynamically changing techniques making their activities more effective. The hackers- act both alone and in a group. Their objective is more than personal benefit. Some common ways fraudsters operate include:

Impersonation: Fraudsters may impersonate legitimate individuals or organizations to gain access to sensitive information or money.

Phishing: It refers to sending fraudulent emails, text messages, or phone calls to trick individuals into giving away personal information or money.

Identity theft: This involves stealing an individual’s personal information, such as their name, address, and social security number, to carry out fraudulent activities.

Credit card fraud: Fraudsters may steal information or use counterfeit cards to make unauthorized purchases.

Ponzi schemes: It uses new investors’ funds to pay off earlier investors in a scheme that promises high returns but is not sustainable.

Money laundering: This disguises the proceeds of illegal activities as legitimate funds by funneling them through various transactions and accounts.

Cybercrime: This involves using technology to carry out various types of fraud, such as hacking into computer systems, installing malware, or using ransomware to extort money.

Insight into Machine Learning Role in the Banking Sector

Machine learning techniques can be used across several aspects, such as loan applications or transactions in the banking and finance sector. Moreover, AI is used in fraud analytics in more than one aspect simultaneously by enhancing how it identifies data abnormalities over time.

Look at some of the common AI applications in the banking sector:

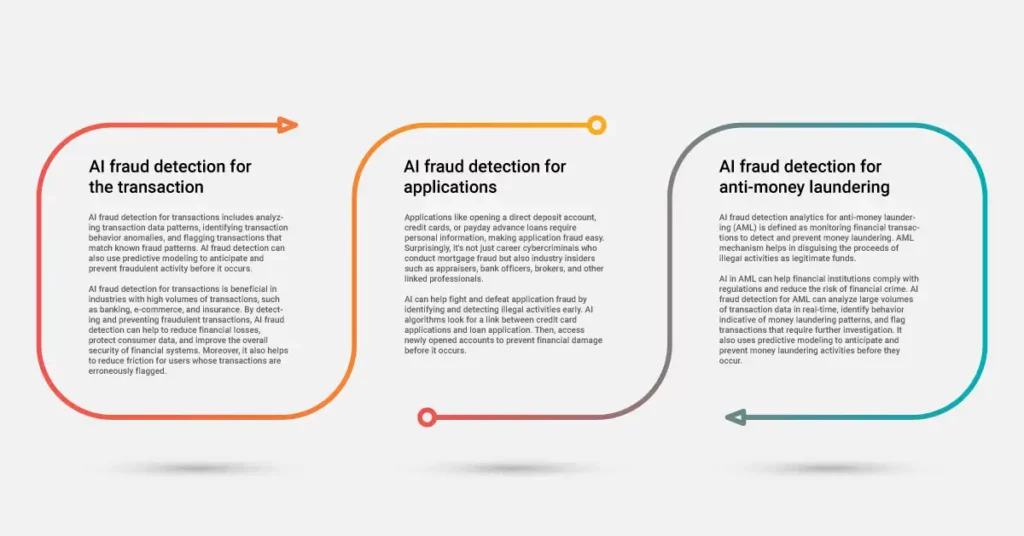

AI fraud detection for the transaction: AI fraud detection for transactions includes analyzing transaction data patterns, identifying transaction behavior anomalies, and flagging transactions that match known fraud patterns. AI fraud detection can also use predictive modeling to anticipate and prevent fraudulent activity before it occurs.

AI fraud detection for transactions is beneficial in industries with high volumes of transactions, such as banking, e-commerce, and insurance. By detecting and preventing fraudulent transactions, AI fraud detection can help to reduce financial losses, protect consumer data, and improve the overall security of financial systems. Moreover, it also helps to reduce friction for users whose transactions are erroneously flagged.

AI fraud detection for applications: Applications like opening a direct deposit account, credit cards, or payday advance loans require personal information, making application fraud easy. Surprisingly, it’s not just career cybercriminals who conduct mortgage fraud but also industry insiders such as appraisers, bank officers, brokers, and other linked professionals.

AI can help fight and defeat application fraud by identifying and detecting illegal activities early. AI algorithms look for a link between credit card applications and loan application. Then, access newly opened accounts to prevent financial damage before it occurs.

AI fraud detection for anti-money laundering: AI fraud detection analytics for anti-money laundering (AML) is defined as monitoring financial transactions to detect and prevent money laundering. AML mechanism helps in disguising the proceeds of illegal activities as legitimate funds.

AI in AML can help financial institutions comply with regulations and reduce the risk of financial crime. AI fraud detection for AML can analyze large volumes of transaction data in real-time, identify behavior indicative of money laundering patterns, and flag transactions that require further investigation. It also uses predictive modeling to anticipate and prevent money laundering activities before they occur.

Why Using AI for Fraud Detection Important?

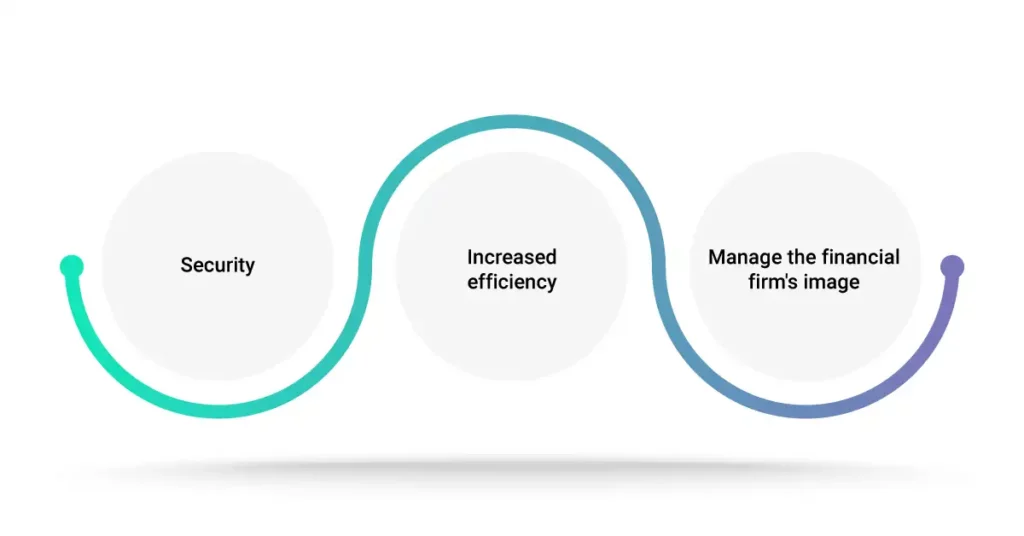

With advanced analytics, you can scan the process of fraudulent activities and further detect the correlation between fraudulent activities and customer behaviors. Some benefits are:

Security: Fraud detection systems function beyond actual funds, as they decrease the probability of tying the business knot with risky partners and find out illegitimate users—advanced analytics help to look at the bigger picture when analyzing inquiries, documents, and applications.

Increased efficiency: AI automates data processing, reducing the stress of manual handling, which is less efficient with the large quantity of information. The developers or data scientists must focus on resolving more complex cases and dive deeper rather than dealing with tons of data.

Manage the financial firm’s image: Several fraud activities impact the business and its customers. With fraud analytics, companies can uphold customer trust by managing their image losses.

Factors while developing an AI-driven Strategy for Banking Fraud Analytics

A few essential factors to consider when developing an AI-driven strategy are:

The dataset:

Imbalance of the dataset: This is a significant concern that data scientists and developers face today. To differentiate between simple operations and fraudulent activities, the model needs sufficient examples to draw the patterns from. This is alarming, looking at the ratio of the positive and negative classes.

Large-sized and good-quality dataset: This is required to learn effectively. This means the complexity of the machine learning model must increase as a single one will not process all the information with the necessary outcomes.

Confidentiality: Financial organizations are not happy to share their datasets as it may cause a data breach. This is because the entity will face confidentiality issues as the data concerns its users directly.

2. The dynamically changing environment: Fraudsters are becoming sophisticated daily and changing strategies at a fast pace to increase their success rate. This forces organizations to regularly retrain their fraud detection algorithms to tackle fraud activities. Hence, a well-developed machine learning model can detect fraudulent activities even if they change their “style” over time.

The Future of Fraud Detection Analytics

The increasing number of frauds and crimes in the banking and financial sector has compelled companies to include a robust solution. Advanced analytical tools and technologies such as data analytics, machine learning, and artificial intelligence help build up the framework and increase operational efficiency. Moreover, the features of a successful fraud detection system include regulatory friendly, customer and manager friendly, scalable, ready for the future, reliable, and can minimize risk.

WRITTEN BY

Team Eela

TechEela, the Bedrock of MarTech and Innovation, is a Digital Media Publication Website. We see a lot around us that needs to be told, shared, and experienced, and that is exactly what we offer to you as shots. As we like to say, “Here’s to everything you ever thought you knew. To everything, you never thought you knew”